After a few turbulent years, financial markets were more settled during 2024 and the value of the UKRF’s assets increased slightly. The year also saw inflation – the increase in the cost of goods and services – fall sharply and interest rates start to come down slowly.

We’re pleased to confirm that the UKRF’s funding level remains strong, with only a slight reduction from the previous year.

2024 was another ‘interim check’ year

We review the UKRF’s finances every year. The 2022 review was our three-yearly, in-depth review (an actuarial valuation) and this year was a lighter, interim check – just to make sure things are progressing as expected. Here’s what we found:

We’re still in surplus

Our 2022 actuarial valuation showed that the UKRF had a funding surplus (learn what this means below).

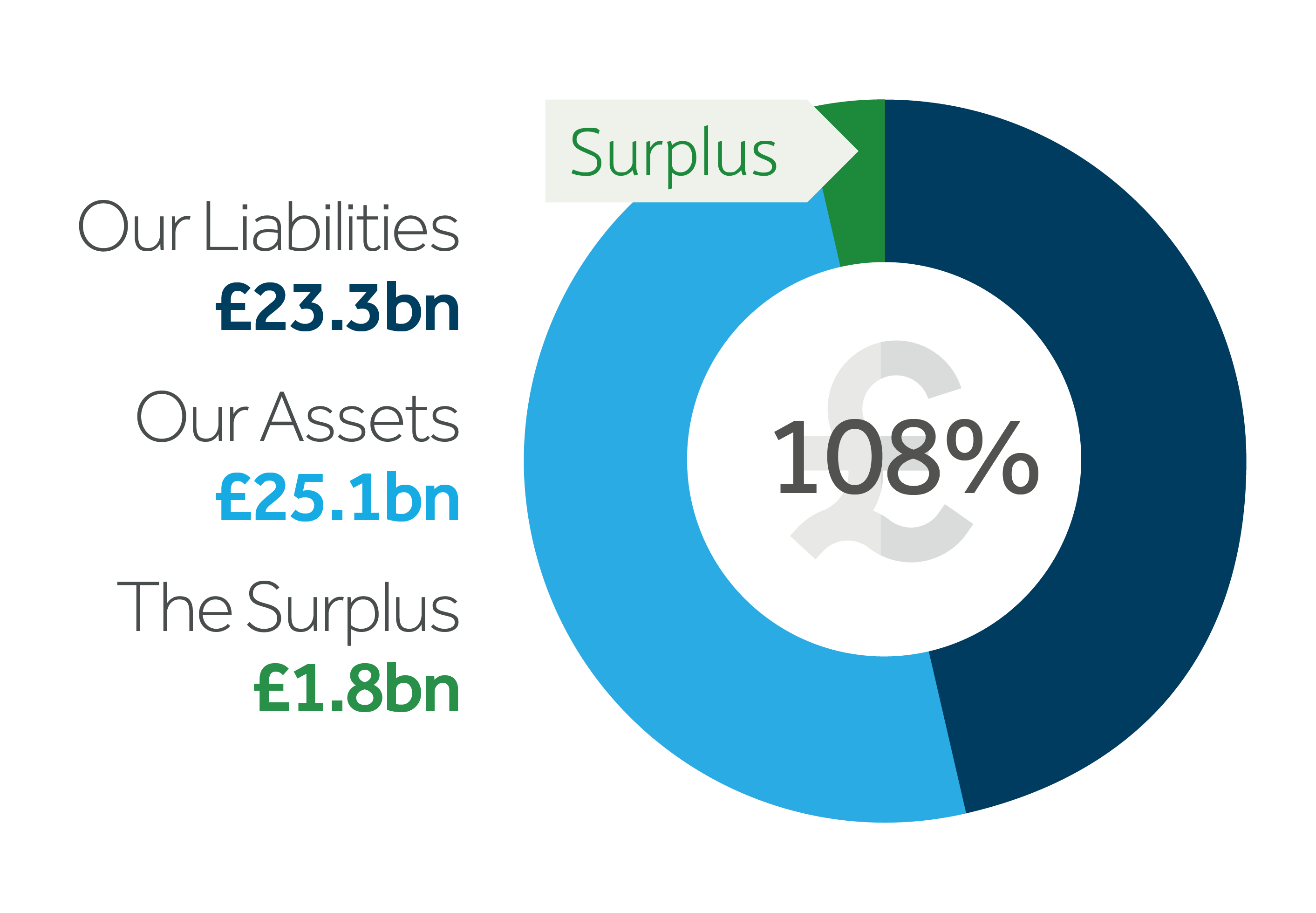

Our 2024 check showed that the UKRF was still in surplus, although that surplus had decreased slightly to £1.8 billion. Our funding level (which measures our assets compared to our liabilities) fell slightly during the year to 108% (down from 109% in 2023).

What’s changed?

Compared to last year, the value of the UKRF’s assets increased slightly. This was offset by an increase in the value of liabilities (the benefits built up by members). This modestly higher value reflects market conditions over the period and the pause in Barclays' contributions.

Keeping our reliance on Barclays low

We know that the UKRF needs to pay benefits for many years to come and that our funding level may fluctuate in the future.

That’s why we’re continuing to focus on maintaining our current strong funding position and making sure our reliance on Barclays support remains low.

Spotlight: What is a ‘funding surplus’?

To answer this question, you first need to know that an actuarial valuation (or interim check) is a calculated estimate. A valuation is worked out at a fixed point in time and looks at how much the UKRF is likely to have in assets compared to how much it expects to pay in members’ benefits, both now and in the future. Independent experts (actuaries) help the Trustee make these estimates by assessing lots of factors like life expectancy trends, and economic and market conditions.

The UKRF is in ‘surplus’ when the value of its assets is expected to be higher than the value of its liabilities. This surplus depends on circumstances at the time; it’s not a fixed value. If there’s a change in any of the assumptions about the underlying factors affecting the value of the UKRF’s finances (life expectancy, economic forecasts etc), the gap (surplus or deficit) between asset and liability values will change too.

We’ve agreed a continued pause on Barclays’ contributions

Following our 2022 actuarial valuation, given the strong funding position, we agreed to Barclays’ request to pause its contributions for 12 months and to carry out a test at 30 September each year to decide if this pause on contributions can continue. After carrying out this test in 2023 and 2024, using the same strict enhanced low-dependency conditions as we did for the initial request, we confirmed that this pause could continue for a further 12 months.

This means that the contributions Barclays would normally make towards members’ benefits (including matching Afterwork contributions) have been met by the UKRF since 1 February 2023. Please be assured that your benefits have not been affected by this decision.

Before agreeing to this request, with the support of our advisers, we reviewed our asset values to make sure they were sufficiently higher than the value of our liabilities. We also wanted to ensure that there was a material 'buffer' and that we could maintain an enhanced low dependency on Barclays. We also checked Barclays’ ability to support the UKRF (its employer covenant) and were confident it remained strong.

A steadfast support

Barclays continues to uphold its overall responsibility as the sponsor for the UKRF. Changes to the UKRF that are intended from 1 July 2025 mean this responsibility will continue to be met by the sponsoring employers of the two Sections of the UKRF: Barclays Bank UK PLC for the Barclays UK Section and Barclays Bank PLC for the Barclays Bank Section. In addition, if either of the sections are estimated to have a funding deficit again, the relevant sponsoring employer will provide a pool of assets as security, which we can use if needed.

What about our investments?

We invest the UKRF’s Defined Benefit assets on behalf of members. Here is how they did over three different time periods to 30 September 2024.

| Total returns to 30 September 2024 | 1 year | 3 years, annualised | 5 years, annualised |

|---|---|---|---|

| These figures only show the return from invested assets. They exclude the effect of money paid out (e.g. pension payments) or money paid in (e.g. contributions from Barclays). | |||

| Total returns to 30 September 2024Total investment returns | 1 year6.2% | 3 years, annualised-9.5% | 5 years, annualised-5.0% |

| Total returns to 30 September 2024Liability returns | 1 year7.1% | 3 years, annualised-11.8% | 5 years, annualised-6.9% |

The ‘liability returns’ are the returns that UKRF assets need to achieve to maintain the funding position.

And finally, by law, we need to tell you:

- • Barclays has not received any money back from the Fund since the 2022 Summary Funding Statement.

- • The UKRF has not received any directions from the Pensions Regulator to change contributions or benefits, nor has the Pensions Regulator made any modifications to the Fund.

- • If the UKRF were to discontinue or ‘wind up’, members’ benefits would need to be secured with an insurance company (instead of by the UKRF). The cost of providing pensions in this way is much higher than providing pensions from the UKRF. At 30 September 2022, the value of the UKRF’s assets was more than the estimated amount needed to secure all members’ benefits built up at that date. This surplus was £0.5 billion, meaning there was a funding level of 102% (compared to 82% in 2019). There is no intention to wind up the Fund.