Strategy

It is crucial to think strategically about the climate-related risks and opportunities that will impact the Fund if we are to stand a chance of mitigating the effects of climate change.

Assessing the climate-related risks and opportunities the Fund is exposed to is key to understanding the impact climate change could have on the Fund in the future.

Executive summary

Through analysis, the Trustee has identified that climate-related risks and opportunities potentially impact to some extent all the different asset classes in which the Fund invests. Over time the potential impact of both physical and transition climate risks increases. During the reporting period, climate change may have provided investment opportunities in different asset classes. Though the Trustee is not currently allocating capital to new assets, it continues to assess climate investment opportunities and allocate further capital to existing assets to take advantage of these opportunities.

The Trustee also identified that the Fund has a reasonable degree of resilience to climate-related risks, this was a key outcome of last year’s quantitative climate scenario analysis based on the three different investment strategies considered, and under all five climate scenarios. The resilience was primarily driven by the high level of diversification of assets. Scenario analysis was not repeated in 2022. The Fund’s portfolio has changed during the reporting period as the Trustee has gradually de-risked. It is expected that this de-risking activity has further reduced the Fund’s exposure to climate risks.

What climate-related risks are most likely to impact the Fund?

Each year we carry out a qualitative risk assessment of the asset classes the Fund is invested in. From this we identify which climate-related risks and opportunities could have a material impact on the Fund.

This is an extensive exercise given the broad range of assets in the Fund. To help us with our assessment, we surveyed our investment managers asking them to rate the climate-related risks and opportunities they believe their Fund assets are exposed to.

Read more

The Fund’s defined benefit (DB) investment portfolio is diversified across a range of different asset classes including hedging assets, private and public credit, public (residual) and private equity, property and insurance assets. There are also defined contribution (DC) assets held in the Fund, however these DC arrangements are for a very small number of members and assets and are considered to be immaterial for the purpose of this analysis.

-

DB Sections asset allocations

Read more

Asset Class Main Section AA Section NWM Section RBSI Section Allocation (%) as at 31 Dec 22 Asset ClassHedging assets Main Section45% AA Section41% NWM Section47% RBSI Section57% Asset ClassCredit1 Main Section26% AA Section34% NWM Section28% RBSI Section31% Asset ClassEquity2 Main Section9% AA Section2% NWM Section6% RBSI Section6% Asset ClassProperty Main Section6% AA Section0% NWM Section5% RBSI Section4% Asset ClassInsurance Main Section3% AA Section6% NWM Section0% RBSI Section0% 1 Includes quoted and private credit securities.

2 Includes residual quoted equity as well as private and alternative equity securities.

-

DC Section asset allocation

Read more

As mentioned above, the Fund has a very small number of DC members and DC assets represent a small proportion of Fund assets membership and for this reason, DC assets have been excluded from the analysis on the basis that they are not material to overall Fund strategy.

How the risk assessment works

-

Risk categories

Read more

In the analysis, the climate-related risks have been categorised into physical and transition risks.

- Transition risks are associated with the transition towards a low-carbon economy. For example, shifts in policy, technology or supply and demand in certain sectors.

- Physical risks are associated with the physical impacts of climate change on companies’ operations. For example, extreme temperatures, floods, storms or wildfires.

Greenhouse, Cambridgeshire. Uses ground source heat pumps and reduces reliance food miles.

Image by Greencoat Capital.

-

Ratings

Read more

The analysis uses a RAG rating system where:

Red

Reddenotes a high level of financial exposure to a risk.  Amber

Amberdenotes a medium level of financial exposure to a risk.  Green

Greendenotes a low level of financial exposure to a risk. -

Time horizons

Read more

The Trustee assessed the climate-related risks and opportunities over multiple time horizons. The Trustee has decided the most appropriate time horizons for the Fund are:

- Short term: up to year 2025

- Medium term: up to year 2035

- Long term: up to year 2050

When deciding the relevant time horizons, the Trustee has taken into account the liabilities of the Fund and its obligations to pay benefits.

Key conclusions

Diversification across asset classes, sectors and regions is important to manage climate-related physical and transition risks for the Fund.

Hedging assets, which are a significant part of the Fund’s assets, are deemed a low-risk area in terms of exposure to climate-related risks, indicated by the green and amber ratings over all time horizons.

Overall, the Trustee has taken proactive steps over the year to mitigate climate-related risks across different asset classes, including:

Read more

- Close monitoring of stewardship activities for credit securities carried out by EOS on behalf of the Trustee with its investment managers (to ensure they are appropriately engaging with investee companies on the management of climate risks);

- Utilising actively managed strategies, such as alternative equity investments into forestry and renewable energy, where appropriate (allowing greater scope to select investments whilst accounting for climate-related risks and opportunities); and

- Integrating climate considerations into all fund reviews and selections, including the appointment of managers with specific sustainability and climate objectives.

Property is a high-risk area, particularly in relation to physical climate risks. The static nature of property investments presents a risk to the Fund, particularly if they are in regions that are vulnerable to climate change. The Trustee has chosen to diversify its investments globally which will help mitigate these risks. All of the Fund’s property managers have provided assurance to the Trustee that they are accounting for these physical risks by not investing in properties in high-risk regions.

The Trustee is also cognisant of the effects climate-related risks may have on the strength of its sponsor covenant. The Trustee’s covenant adviser, Penfida, monitors covenant strength on an ongoing basis, reporting to the Trustee quarterly, and are increasingly considering climate-related risks in their assessment and advice.

For a more detailed risk assessment by asset class please see below.

Climate-related risks and opportunities

Climate-related risk assessment

The summary of the assessment for each asset class is captured below. In every asset class, the Trustee works closely with the managers to understand their risk exposure and the mitigations being undertaken.

| Physical risks | Transition risks | |||||

|---|---|---|---|---|---|---|

| Time horizon | Physical risksAcute | Physical risksChronic | Transition risksRegulatory | Transition risksTechnology | Transition risksMarket | Transition risksReputation |

| Short | Physical risks - acute |

Physical risks - chronic |

Transition risks - regulatory |

Transition risks - technology |

Transition risks - market |

Transition risks - reputation |

| Medium | Physical risks - acute |

Physical risks - chronic |

Transition risks - regulatory |

Transition risks - technology |

Transition risks - market |

Transition risks - reputation |

| Long | Physical risks - acute |

Physical risks - chronic |

Transition risks - regulatory |

Transition risks - technology |

Transition risks - market |

Transition risks - reputation |

The Fund’s hedging assets are invested in UK Government bonds, cash instruments and swaps to manage risk versus the Fund’s liabilities. These assets provide a good level of protection against interest and inflation rate changes that might arise from climate-related risks (for example, inflation caused by higher asset costs that could arise from climate-related transition risks).

The above risk assessment has been updated from the previous year to reflect the hedging manager’s climate-related views. There are no substantial changes since last year’s assessment. The manager does not see material financial impacts in the short-term and medium-term. These risks are relatively geographically concentrated and not expected to have material financial impact on UK sovereign bonds, although there is some risk over the longer-term. Policy changes such as carbon pricing will cause demand patterns to shift over the medium and long-terms and may be accompanied by changing market sentiment independent of policy change. It is likely that many fossil fuel exporting countries see relatively larger losses in GDP, depending on the ambition of global policy and resulting demand patterns. As a result, they may see their credit ratings fall and yields increase, with some impact on investors’ global sovereign bond portfolios.

In light of the analysis above, the Trustee is comfortable with the current hedging strategy and is of an opinion that hedging instruments (UK gilts in particular) are less affected by climate-related risks compared to other return seeking assets classes.

| Physical risks | Transition risks | |||||

|---|---|---|---|---|---|---|

| Time horizon | Physical risksAcute | Physical risksChronic | Transition risksRegulatory | Transition risksTechnology | Transition risksMarket | Transition risksReputation |

| Short | Physical risks - acute |

Physical risks - chronic |

Transition risks - regulatory |

Transition risks - technology |

Transition risks - market |

Transition risks - reputation |

| Medium | Physical risks - acute |

Physical risks - chronic |

Transition risks - regulatory |

Transition risks - technology |

Transition risks - market |

Transition risks - reputation |

| Long | Physical risks - acute |

Physical risks - chronic |

Transition risks - regulatory |

Transition risks - technology |

Transition risks - market |

Transition risks - reputation |

Credit is the Fund’s second-largest allocation and includes a broad spectrum of investments, such as investment grade securities, distressed credit, real estate debt and infrastructure debt investments.

Credit markets have a high exposure to transition risk. Issuers that are slower to participate in the transition to a low carbon economy are likely to face reputational damage. Also, the potential for unexpected and aggressive emissions regulation may create higher costs (e.g., carbon taxes) for companies. Unanticipated regulation could leave some sectors with significant stranded assets. These and other transition risks could lead to increased risk of downgrade or default.

In the near-term, transitional risks are far less evident for emerging markets assets and entities, where solid legislation and regulation around greenhouse gas emissions (GHG) are generally not yet present. Substitution and transition to cleaner energy require alternatives and these are still in the early stages of development. However, the risks are anticipated to be more pronounced in the future, as efforts to reduce climate change are embraced globally and not just in the developed world.

The Trustee mitigates transitional risk by not owning investment grade oil and gas debt with a maturity greater than 2025 and not lending to entities where more than 50% of revenue is derived from extraction of thermal coal.

There have been some changes in credit managers’ climate risk assessment since last year, for example, all six risk factors identified now have an amber rating for the medium-term (where previously, acute, chronic, technology, and reputation were rated green). Over the medium-term, acute, chronic, technology and reputation risks have received amber ratings (compared to green ratings last year). Over the long-term period, technology has received an amber risk rating (where this was red previously) and chronic has received a red risk rating (which was amber last year).

Overall, the Trustee recognises that physical events due to climate change are becoming more frequent and more impactful and the Trustee is ultimately comfortable with the analysis and the Fund’s allocation to credit strategies.

| Physical risks | Transition risks | |||||

|---|---|---|---|---|---|---|

| Time horizon | Physical risksAcute | Physical risksChronic | Transition risksRegulatory | Transition risksTechnology | Transition risksMarket | Transition risksReputation |

| Short | Physical risks - acute |

Physical risks - chronic |

Transition risks - regulatory |

Transition risks - technology |

Transition risks - market |

Transition risks - reputation |

| Medium | Physical risks - acute |

Physical risks - chronic |

Transition risks - regulatory |

Transition risks - technology |

Transition risks - market |

Transition risks - reputation |

| Long | Physical risks - acute |

Physical risks - chronic |

Transition risks - regulatory |

Transition risks - technology |

Transition risks - market |

Transition risks - reputation |

The assessment has been undertaken in relation to private and ‘alternative’ equity, which taken together, are the Fund’s third largest asset class exposure. The Fund has divested from the majority of its quoted equity holdings reducing the Fund’s exposure to market and reputation risks associated with climate change.

Of relevance from a climate risk and opportunity perspective is the Fund’s allocation to global forestry, within alternative equity. Alongside the return and diversification benefits of this asset class, it also provides two valuable climate-related features. Firstly, by employing sustainable harvest practices, the forests provide a carbon sink which offsets emissions elsewhere in the portfolio, and secondly the value of the other (harvested) forests is expected to benefit from both increasing carbon prices and demand for timber as a lower-carbon substitute for other materials. Nonetheless, the Trustee also recognises that forestry is becoming more exposed to wildfires. The Trustee believes that the forest management to mitigate climate-related risks may call for adaptation of silvicultural practices, as well as technological interventions, to enable improved prediction and identification of extreme weather events. Another opportunity the Fund benefits from is in relation to renewable energy via wind farms, waste to energy and anaerobic digestion. The Trustee values these investments due to their positive environmental benefits and contribution to reducing the UK’s reliance on fossil-fuel energy generation.

Following the equity managers’ reassessment of climate-related risks, short-term regulatory risk, medium-term market risk, and long-term chronic and technology risks have now been rated amber, in comparison to a green rating assigned last year. This indicates higher prevalence of climate-related risks for the alternative equity.

| Physical risks | Transition risks | |||||

|---|---|---|---|---|---|---|

| Time horizon | Physical risksAcute | Physical risksChronic | Transition risksRegulatory | Transition risksTechnology | Transition risksMarket | Transition risksReputation |

| Short | Physical risks - acute |

Physical risks - chronic |

Transition risks - regulatory |

Transition risks - technology |

Transition risks - market |

Transition risks - reputation |

| Medium | Physical risks - acute |

Physical risks - chronic |

Transition risks - regulatory |

Transition risks - technology |

Transition risks - market |

Transition risks - reputation |

| Long | Physical risks - acute |

Physical risks - chronic |

Transition risks - regulatory |

Transition risks - technology |

Transition risks - market |

Transition risks - reputation |

Property exposure is diversified across the UK, the US and Europe and are likely to be impacted by a combination of physical and transition risks. Physical risks arising from climate change could lead to property damage and material financial impacts, particularly in geographically vulnerable areas.

The principal physical climatic risk experienced in the UK is fluvial flooding. Through its holdings in the US, the property portfolio is also exposed to other physical risks such as hurricanes and wildfires.

Transition risks, such as tenants preferring ‘green’ buildings and therefore making some buildings effectively ‘un-rentable’, are significant climate-related issues. Other examples include energy efficiency regulations, increases in energy costs, carbon taxes, and valuation considerations that could lead to increased costs.

The Trustee prohibits new investments in properties that have a high flood risk. The Trustee encourages managers to design new properties with the objective of producing zero emissions once they are operational, such as its investment in the construction of retirement villages in the UK. Managers of existing commercial properties are required to continually improve the operational efficiency of the buildings owned by the Fund and put a plan in place to attain higher energy efficiency ratings in order to mitigate the risk of stranded assets.

There have been some updates to the property managers’ climate risk assessment since the previous year. Mainly, short-term regulatory risk has now been rated amber, where this was previously green. Medium-term market, technology and reputation risk have now been rated amber, where they were previously green. The medium-term chronic risk rating on the other hand has been allocated a green risk rating (compared to amber last year). Over the long-term, both the acute and chronic risks have received amber ratings (compared to red ratings last year), and technology has received an amber rating (which was previously green). Property managers are exhibiting greater levels of climate change considerations in their constructions and management of properties, which has been positively reflected in their exposure to climate-related risks over longer time horizons. Overall, the Trustee is comfortable with the analysis and the Fund’s allocation to its property investments.

| Physical risks | Transition risks | |||||

|---|---|---|---|---|---|---|

| Time horizon | Physical risksAcute | Physical risksChronic | Transition risksRegulatory | Transition risksTechnology | Transition risksMarket | Transition risksReputation |

| Short | Physical risks - acute |

Physical risks - chronic |

Transition risks - regulatory |

Transition risks - technology |

Transition risks - market |

Transition risks - reputation |

| Medium | Physical risks - acute |

Physical risks - chronic |

Transition risks - regulatory |

Transition risks - technology |

Transition risks - market |

Transition risks - reputation |

| Long | Physical risks - acute |

Physical risks - chronic |

Transition risks - regulatory |

Transition risks - technology |

Transition risks - market |

Transition risks - reputation |

The Fund invests in insurance-related funds covering a wide range of insurance risks.

Due to the nature of most insurance contracts the Fund invests in, there are no notable climate-related risks. However, the strategy has indirect immaterial exposure to physical risks through its holdings of catastrophe insurance linked securities. The Trustee does not believe these pose material issues in terms of its climate-related risks considerations.

Climate-related opportunities

The Fund has been closed to new members since 2006 and therefore the assets and liabilities will decline significantly over the next 30 years. The Trustee employs a low-risk investment strategy with high levels of hedging and has approved a strategy targeting buy-in for its Main and AA Sections which limits the Trustee’s ability to make new investments. The Trustee believes that the best way to access climate opportunities is through improving the operations of its existing assets and making selected capital expenditure in existing assets where this will provide a financial return over the Fund’s expected investment period.

The Trustee does recognise that there is a vast array of climate-related opportunities available, which are summarised below. The Trustee has already taken advantage of some of these opportunities as part of its investment strategy.

-

Cleaner energy

Green power generation, clean technology innovation, sustainable biofuels

-

Environmental resources

Water, agriculture, waste management

-

Energy and materials efficiency

Advanced materials, building efficiency, power grid efficiency

-

Environmental services

Environmental protection, business services

Lowering fuel consumption from the installation of rotor sails in bulk carrier vessels.

Image from Tufton Investment Management Ltd.

How resilient is the Fund to climate change?

To get a better understanding of the impact climate change could have on the Fund’s assets and liabilities, the Trustee has looked at how the Fund might perform under different climate change scenarios.

Read more

The Trustee has looked at five different climate change scenarios. Each scenario considers what might happen when transitioning to a low carbon economy under different conditions. The Trustee chose these scenarios because it believes that they provide a reasonable range of possible climate change outcomes.

These scenarios were developed by Aon and are based on detailed assumptions. They are only illustrative and are subject to considerable uncertainty. Aon established a “base case” scenario against which the five climate change scenarios are compared.

Potential impact of climate change

Click on the different transition scenarios to understand the impact of climate change.

- Smooth transition < 1.5℃

- Base scenario + 2℃ - 2.5℃

- Abrupt transition +< 2℃

- Orderly transition +< 2℃

- Disorderly transition + 3℃ - 4℃

- No transition >4℃

Considers the impact when the private sector innovation and a green technology revolution, combined with government coordination, help drive progress towards tackling climate change.

Emission reductions start immediately and continue in a measured way in line with the objectives of the Paris Agreement and the UK Government’s legally binding commitment to reduce emissions in the UK to net zero by 2050.

Explores the impact of delayed action on climate change for five years with governments eventually forced to address GHG emissions due to increasing extreme weather events.

Considers the impact of immediate and coordinated action to tackle climate change using carbon taxes and environmental regulation.

Considers the impact of climate change if insufficient sustainable policy action is undertaken to manage global temperatures effectively over the next 10 years.

Considers the impact when the world economy remains oriented towards improving near-term economic prospects, with companies and governments taking a "business as usual" approach.

Summary of the analysis

Based on the climate scenario analysis, the following conclusions were drawn:

- The Main Section’s investment portfolio and funding level exhibits good resilience under the climate change scenarios due to high diversification of assets, low proportion of equities and high levels of hedging against changes in interest rates and inflation.

- NWM and RBSI Sections also demonstrate reasonable resilience under the climate change scenarios.

- Overall, climate risks are the lowest for the AA Section due to the absence of quoted/private equity.

After reviewing the climate scenario analysis, the Trustee is comfortable that the Sections display sufficient resilience to the potential impacts of climate change as envisaged by Aon’s proprietary models, and at this stage are not proposing any material changes to investment strategy as a result.

Whilst the scenario analysis indicates that, even under adverse climate scenarios, the funding level of the various Sections is relatively resilient, the Trustee will use the analysis when considering sponsor covenant and the impact of possible future funding shocks.

The Trustee will review the appropriateness of the climate scenario analysis on an annual basis with the next review expected to take place in January 2024. The Trustee expects to update the climate scenario analysis at least triennially – this may be undertaken sooner if there are material developments affecting the Fund (or each Section), which would include any changes to the strategic asset allocation.

Please note that the key scenario analysis assumptions have been set out in the 'Appendix – Climate scenario modelling assumptions'.

Climate impact assessment

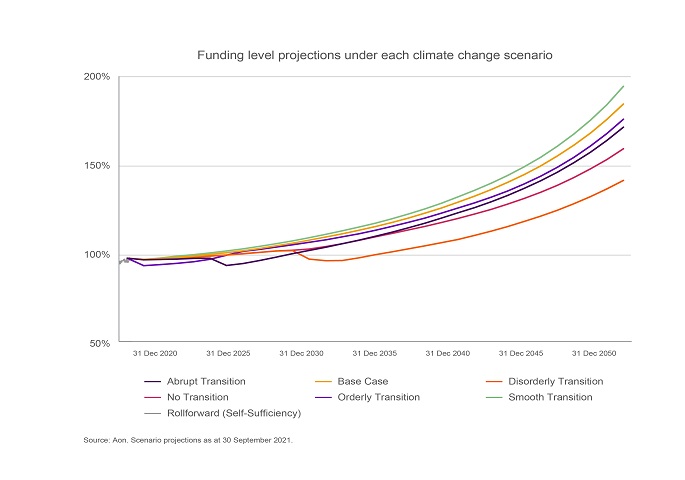

The Fund’s investment portfolio exhibits good resilience under the climate scenarios over the 30-year projection period. This is due to the diversification of assets, low proportion of equities1 and high levels of hedging against changes in interest rates and inflation.

The worst-case scenario for the Main Section is the disorderly transition. Although initially the funding level improves (albeit at a slower rate than the base case), after 10 years the funding level deteriorates modestly. Although the Section is left materially worse off relative to the base case by the end of the modelling period, there is still expected to be a positive funding surplus. The strong starting position and diversified strategy reduces the downside impact of the disorderly scenario on the Fund.

Despite the resilience of the investment strategy, the funding level is volatile under some of the scenarios. For example, under the abrupt transition the Fund experiences a c. 4% fall in the funding level, which leads to a lag in the time taken to reach full funding, relative to the base case, of around seven years. Deterioration of the funding level may place a strain on the sponsor covenant as they may have to make up a bigger shortfall through deficit contributions. It may also require the Fund to re-risk in order to stay on track to achieve the funding target, or extend the timeframe for achieving this.

Funding level projections under each climate change scenario

Source: Aon. Scenario projections as at 30 September 2021.

1 Equities were divested from over the year.

Note that the modelling assumes the current investment strategy remains unchanged over time. It does not allow for future changes the Trustee might make as the liabilities mature.

What do the charts show?

The charts show what might happen to the Fund’s DB funding level under each climate scenario up to 30 years into the future. Each line represents a different scenario.

The funding level is a measure of how much surplus assets (or deficit) the Fund has above the cost of the pension liabilities.

Depending on the scenario, the funding level increases more or less. Under some scenarios the funding level experiences sudden falls.

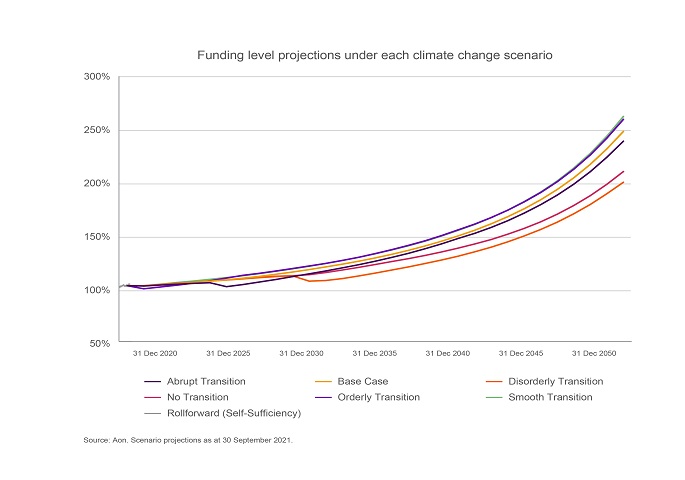

The AA Section’s investment portfolio displays strong resilience to climate change risk over the 30-year projection period. This is due to the absence of traditional equity in the portfolio, as well as the high levels of hedging to protect against changes in interest rates and inflation.

As with Main Section, the worst-case scenario for the AA Section is the disorderly transition. However, owing to the strong starting funding position and the more defensive investment strategy, the downward shock is not sufficient to reduce funding to below 100% after several years of growing surplus. Although the Fund is again left materially worse off relative to the base case by the end of the modelling period, the strong starting position and low risk strategy mitigates the downside impact on the Fund.

One key difference relative to the Main Section is the muted impact of the orderly transition scenario. This reflects the smaller allocation to non-credit growth assets (and notably the absence of traditional equity). The muted funding drop leaves the Fund in a strong position to benefit from stronger post-transition returns, with funding (under the orderly scenario) overtaking the base case from year five onwards. Given the full funding position on this Section, the climate scenario analysis suggests that the impact on the funding level will be muted.

Funding level projections under each climate change scenario

Source: Aon. Scenario projections as at 30 September 2021.

Note that the modelling assumes the current investment strategy remains unchanged over time. It does not allow for future changes the Trustee might make as the liabilities mature.

What do the charts show?

The charts show what might happen to the Fund’s DB funding level under each climate scenario up to 30 years into the future. Each line represents a different scenario.

The funding level is a measure of how much surplus assets (or deficit) the Fund has above the cost of the pension liabilities.

Depending on the scenario, the funding level increases more or less. Under some scenarios the funding level experiences sudden falls.

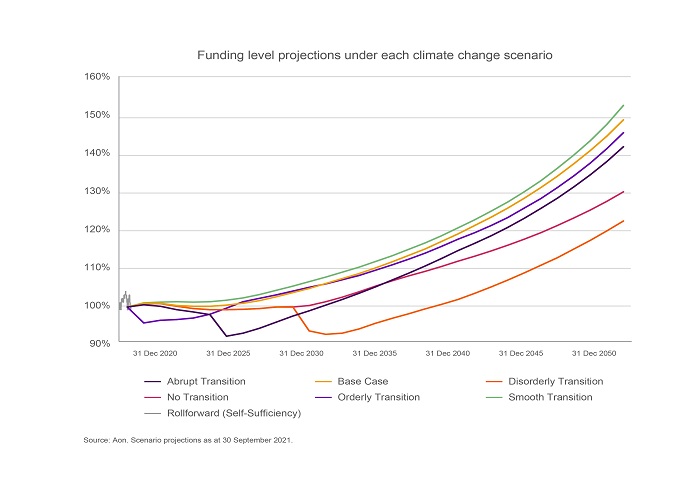

The Fund’s investment portfolio exhibits some resilience under the climate scenarios. As with the Main Section, this is due to the low proportion of equities1 and high levels of hedging to protect against changes in interest rates and inflation.

As with the Main and AA Sections, the worst-case scenario for the NWM Section is the disorderly transition. However, the higher proportion in growth assets results in the Fund being more exposed to climate risks than the other two Sections (even though much of the growth allocation is in credit). This results in a slightly larger funding drop under the disorderly transition scenario than is seen for the other two Sections, with the funding level falling significantly during the transition.

The downside climate risk is also demonstrated under the orderly/abrupt transition scenarios, but subsequent recoveries are borne out much earlier than under the disorderly transition. This allows funding to recover much closer to the base case by the end of the 30-year modelling period. Deterioration of the funding level may place a strain on the sponsor covenant as they may have to make up a bigger shortfall through deficit contributions. It may also require the Fund to re-risk in order to stay on track to achieve the funding target, or extend the timeframe for achieving this.

Funding level projections under each climate change scenario

Source: Aon. Scenario projections as at 30 September 2021.

1 Equities were divested from over the year.

Note that the modelling assumes the current investment strategy remains unchanged over time. It does not allow for future changes the Trustee might make as the liabilities mature.

What do the charts show?

The charts show what might happen to the Fund’s DB funding level under each climate scenario up to 30 years into the future. Each line represents a different scenario.

The funding level is a measure of how much surplus assets (or deficit) the Fund has above the cost of the pension liabilities.

Depending on the scenario, the funding level increases more or less. Under some scenarios the funding level experiences sudden falls.

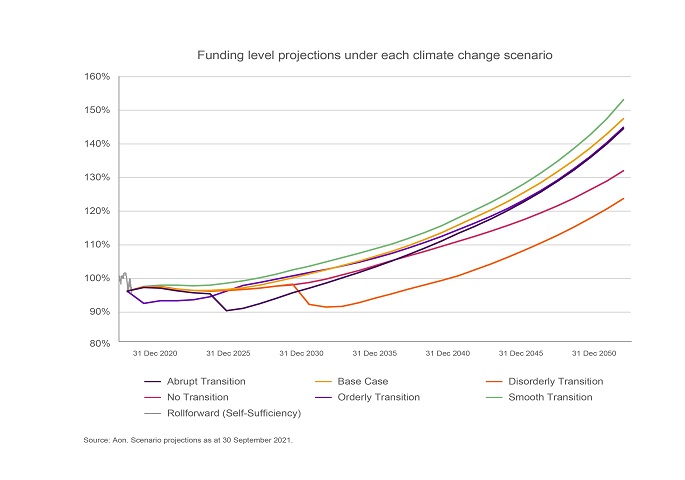

The RBSI Section’s investment portfolio exhibits some resilience under the climate scenarios. As with the Main and NWM sections, this is due to the low proportion of equities1 and high levels of hedging to protect against changes in interest rates and inflation.

As with the Main, AA and NWM Sections, the worst-case scenario for the RBSI Section is the disorderly transition. The pattern seen is very similar to the NWM Section, with the funding level dropping significantly as the transition occurs. Again, this reflects the higher proportion of growth assets when comparing to the Main or AA Sections.

The slightly higher exposure to climate risks is also seen under the abrupt transition scenario, with full funding delayed relative to the base case after the transition shock. Deterioration of the funding level may place a strain on the sponsor covenant as they may have to make up a bigger shortfall through deficit contributions. It may also require the Fund to re-risk in order to stay on track to achieve the funding target, or extend the timeframe for achieving this.

Funding level projections under each climate change scenario

Source: Aon. Scenario projections as at 30 September 2021.

1 Equities were divested from over the year.

Note that the modelling assumes the current investment strategy remains unchanged over time. It does not allow for future changes the Trustee might make as the liabilities mature.

What do the charts show?

The charts show what might happen to the Fund’s DB funding level under each climate scenario up to 30 years into the future. Each line represents a different scenario.

The funding level is a measure of how much surplus assets (or deficit) the Fund has above the cost of the pension liabilities.

Depending on the scenario, the funding level increases more or less. Under some scenarios the funding level experiences sudden falls.

Developments & data limitations

Read more

Main, NWM and RBSI Sections reduced their allocations to quoted equities over 2022. Rising interest rates resulted in improved funding levels for all Sections of the Fund. Accordingly, funding risk has improved significantly, reducing Trustee exposure to climate risks and to its sponsor. As a consequence, the Trustee has approved a change in strategy for the Main and AA Section(s) to target a buy-in at some point in the future. A buy-in would involve the Trustee passing the assets over to an insurer. In return the Trustee would receive an insurance policy which would deliver cashflows matching the benefit payments the Fund makes to members. This ultimately means that the Trustee would have substantially fewer assets over which it has direct control. Nonetheless, the Trustee has reviewed the appropriateness of the climate scenario analysis from last reporting period and believes that with its new strategic imperative and plans to de-risk the Fund, carrying out further scenario analysis at this stage would not inform its strategic decision making going forwards.

Please note that the Fund has a limited amount of DC members, and DC assets represent only a small proportion of Fund assets. For this reason, DC assets have been excluded from the climate scenario analysis on materiality grounds.